Deepwater Gulf of Mexico: Bright Future

Quest Offshore characterizes the U.S. Gulf of Mexico as a deepwater region that is “Transitioning into a Bright Future.” According to the recently released 116-page Quest Deepwater Review Gulf of Mexico report, the Gulf of Mexico has experienced massive changes in the last 5 years with long-term implications for the region and the wider deepwater oil and gas market. The worldwide financial crisis and subsequent recession, shale gas’ implications on U.S. natural gas prices, the Macondo incident and changes to the regulatory regime have been the prime movers.

Recent discoveries of large deep and ultra-deepwater reserves have drastically increased the reserve and production expectations of the region. Five years ago, the Gulf of Mexico was a region with a mix of major and independent operators executing standalone and subsea tiebacks gas and oil projects. Today, oil dominates the region with offshore gas all but unable to compete in a sub $4/mmcf gas price environment. Many independent operators have exited the region, but some major operators and large independents have increased their exposure, betting on ultra-deepwater projects that promise significant rewards and equally large risks. But, continues Quest, the almost two year halt to drilling activity will have long-term consequences for local industry.

Local investment during the drilling moratorium was helped by the execution of capital intensive stand-alone floating production developments that were delayed from 2008-2010. These projects moved forward without the need of additional drilling. Meanwhile, the mix of well permits for multi-well developments compared to exploration has shifted significantly over the past few years, leading to concerns about the long-term effects of regulatory changes on the future of the region. While major operators have moved past the effects of the drilling moratorium and economic crisis, some smaller independents have moved ashore. At the same time some national oil companies (Petrobras) are exiting the Gulf while new players (Statoil) emerge.

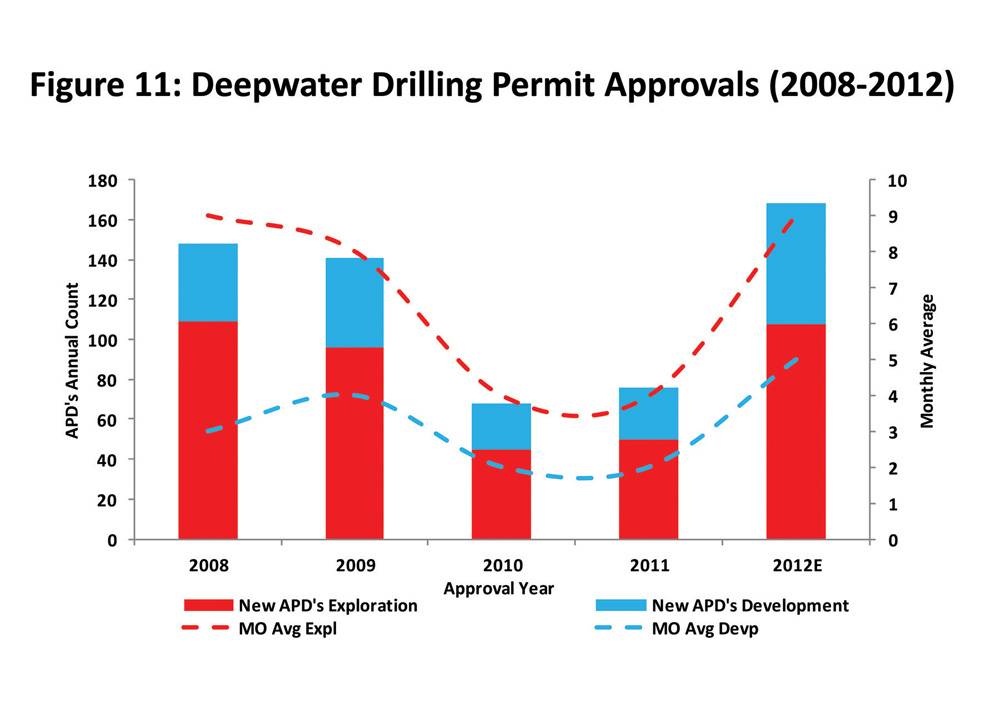

Drilling Market Accelerating: Drilling permit approvals are showing noticeable increases over the past six months with total counts back to pre-Macondo levels. By the end of September, 78 new exploration drilling permits and 36 new development drilling permits were approved over the year. Notable discoveries of ultra-deepwater fields in the Lower Tertiary continue to increase the reserve and production expectations for the region.

The shift in the Gulf is most apparent in the floating rig market with four operators now possessing 50 percent of the contracted rig fleet. The water depth capability shift in the region to favor ultra-deepwater rigs is also significant with 90 percent of rigs operating now ultra-deepwater rigs whereas five years ago 50 percent of rigs were mid-water or deepwater floaters (segments that now make up less than 10% of the contracted fleet). Leasing activity shows similar trends.

Spending is expected to increase significantly starting in 2013 with spending expected to be up 30 percent to $40 billion. Overall expenditures are expected to reach a massive $167 billion between 2013 and 2016. In 2012, deepwater capital and operational expenditures are expected to surpass shallow water capital and operational expenditures for the first time. The deepwater floating and pipeline infrastructure being installed, coupled with the next wave of infrastructure expected to be deployed, will provide development opportunities and establish the next generation of production facilities to support the hub-and-spoke development concept.

Led by the rising number of forecast world class capital projects, availability for high-end marine construction vessels is expected to tighten considerably even within the growing supply base. Over 5,000 km of pipelines are forecast through 2016, a more than 25 percent gain from the previous five years. At year-end 2011, sixty-three thousand metric tons of floating production system (FPS) topside orders were tabulated, marking the highest level in recent years. Moreover, spending on Spar FPS types is projected to increase four-fold to $6.4 billion over the forecast period (2012-2016) compared with the previous five years. Similarly, spending on semi-submersible platforms is forecast to grow to $3.3 billion a nearly 250 percent increase sequentially.

The decommissioning sector in the region is also expected to see a major transformation. Decreased shallow-water installations coupled with high activity driven by recent major hurricanes and the government’s idle iron policy are expected to lead to a larger number of abandonments and a rising trend for decommissioning opportunities. The significant challenges in deepwater removals and abandonments (subsea wells and structures) will translate into higher value contracts than the shallow water work, lending a brighter outlook for companies involved in this market.

Robust Outlook for Deepwater Development: Since 2008, the U.S. Gulf of Mexico has undergone a shift in project development mix from heavy in small, independent--operated subsea tiebacks to one that is grounded in fewer, larger subsea tiebacks and high--investment stand alone developments developed by international oil companies and mega--independents.

Risks to the regions’ future include the uncertain global macro-economic outlook and the implications of government regulations. Nevertheless, operators and contractors dedicated to the region are expected to prosper in the coming years. Those players unable to adapt to the new realities of the region are expected to struggle while those with other, global interests will continue to move out of the Gulf. Also according to Quest, the Gulf of Mexico is expected to continue to be one of the leading deepwater regions in the world for the foreseeable future and to continue to provide a safe source of domestic energy for the United States.

(As published in the December 2012 edition of Marine News - www.marinelink.com)