Logistics Mergers Up, Says KPMG

Auditor KPMG says that the mergers and acquisitions (M&A) in the Transport sector will supersede the levels seen in 2015 this year.

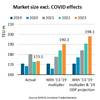

In 2016, mergers and acquisitions (M & A) in the Transport sector will supersede the levels seen in 2015 by exceeding the £ 52 billion mark, according to KPMG's latest Transport Tracker.

The analysis found that the value of completed M & A transactions in 2016 will pass the 2015 mark, which rose for the third consecutive year, to a total of £ 48 billion. Further transactions worth approximately £ 66 billion were announced, hitting a record level of M & A activity in the sector in 2015.

The upcoming year will remain active in terms of investments with trends identified as three main drivers:

1) ASPAC will continue to attract investments as a source of new growth

ASPAC targeted acquisitions contributed to 55% of the announced transaction values in 2015, and we expect this trend to continue reflecting underlying demographics, and the search for new markets. Landmark transactions announced in 2015 included: the operating concession for Kansai and Osaka airports valued at £ 11.7bn; the acquisition of Australian rail and port operator Asciano for £ 4.3bn; and Singapore's Neptune Orient Lines acquisition by CMA CGM for £ 1.4bn.

2) Asset-heavy and asset-light business model convergence in Freight & Logistics

The total value of completed Freight & Logistics M & A transactions have more than quadrupled from £ 7.2bn in 2013 to £ 31.4bn in 2015, and further transactions worth approximately £ 33.2n were announced during the year.Asset-light logistics operators with advanced IT systems have, in recent years, been popular acquisition targets for large logistics providers and freight forwarders. However, we increasingly see that that "leaner" logisticians are looking for assets and (reliable) networks to supplement their services.

Examples include the acquisition of US logistics company Coyote Logistics (high-tech / asset-light business model) by UPS worth £ 1.2bn, and the takeover of the French Norbert Dentressangle forwarder by XPO Logistics for £ 1.8bn.Following the £ 3.3bn acquisition of tOLL Logistics by Japan Post in 2015 (which will transform the business model of the postal service operator towards a full-service logistics provider); the anticipated completion of the FedEx TNT deal (£ 3.1bn) will set the basis for another big year in M & A.

3) Alliance and partnership models will continue to evolve where M & A cannot

M & A activity in the airline sector remained relatively low in 2015 (at £ 3.1 billion of completed transactions) which is primarily because of restrictions imposed by foreign ownership restrictions and regulation.

In the meantime, airlines will continue to evolve their business models and levels of co-operation towards alliance and partnership to optimize their networks, provide increase passenger choice, and pursue growth. Examples of new alliances in 2016 include the JV between Lufthansa and Singapore Airlines, and the alliance between IAG and LATAM.

James Stamp, UK head of transport at KPMG said: "We expect investment activities in the transport and logistics sector to remain high driven by the search for growth; changes in demographics and supply chain; evolution of business models; increased focus on customer proposition, and changes to the regulatory environment.

"With interest rates remaining low, returns on asset acquisitions remain attractive. We expect that further investments this year will see transactions to significantly exceed £ 52bn on the basis of announced transactions alone. "