Does the Container Sector Need to go back to School?

Drewry’s quarterly Container Forecaster focuses on early 2011 and how the scene is being set for what looks like another boisterous year for the sector. What, if any, lessons have been learnt?

London, UK, 13th April 2011 -The basic education of school-children used to revolve around the Three R’s of reading, writing and arithmetic. It seems that the container syllabus is currently following a similar mantra. The 3 R’s of Containerisation = rates, reductions, recklessness.

Having last year successfully overturned the heavy losses of 2009; it looks increasingly likely that carriers will be once again flirting with the red ink come the end of this year.

In December, Drewry forecast that container shipping industry-wide profits will be reduced to $7-8 billion this year, down from the $17 billion bonanza of 2010. However, ill-discipline on rates and capacity management, combined with escalating operating costs means that Drewry now thinks that many carriers will struggle to break even.

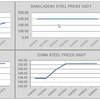

The warning signs were there in the fourth quarter of last year as carriers were unable to sustain the upward momentum in profits of the first three quarters of 2010 as higher costs and some oversupply of tonnage (reducing load factors) kicked in. The erosion in freight rates has continued in the first three months of 2011, which unless checked very shortly could lead to losses at a number of lines at least in the short-term. Drewry’s quarterly Container Forecaster projects that east-west freight rates excluding fuel will fall by 13.2% in 2011.

Perversely, freight rates on the core east-west headhaul trades have been in decline since hitting their highs in August of last year and this is certainly not due to any inherent weakness in demand. An excess of supply and an unfortunate return to the carrier strategy of “chasing market share” has led to spot rates in the transpacific and Asia-Europe trades falling by up to 40-50% during this period.

There is a serious risk that unless spot rates recover in the next 4-6 weeks, recently signed BCO annual rates in the eastbound transpacific might be above the spot market which will lead to re-negotiations. A precursor to the volatility that might lie ahead can be seen with the retrenchment of CSAV in the transpacific and suspension of The Containership Company’s single service in the same trade.

Adding to carriers’ woes are the steep fuel price rises that have intensified during the North African and Mid-East political uprisings. With bunkers now priced at about $650 per tonne, the BAF element of current spot rates on the Asia to North Europe route means that carriers will only have a contribution of $200-300 per teu.

Ocean carriers always struggle to charge a floating BAF in these trades as the all-in pricing mechanism has almost become the standard. It is imperative that carriers try to force these through in the short term if they are not to lose substantial revenue in the next few months.

The industry is well accustomed to profit swings, but if, as seems likely, industry profits vanish this year, it would mark possibly the shortest business cycle container shipping has ever seen. In the space of three short years the industry will have gone from bust in 2009 (-$19 billion) to boom in 2010 (+$17 billion est.) and back to bust (small profit or loss) in 2011.

As mentioned, the prospect of weaker carrier financial statements is not connected to any significant dampening to volumes. From a demand perspective, the current fundamentals look fairly promising with global volumes projected to rise by 8.3% in 2011.

Our preliminary full-year estimate records growth in global port throughput of 13.8% in 2010, lifting the annual volume to a best ever 541.8 million teu, up by 3% on the previous record set in 2008.

It is the supply side of the equation that gives Drewry reason to be cautious regarding carrier profitability.

Carriers decided to cancel individual weekly sailings as their primary means of capacity management this winter, rather than suspend individual strings. Coupled with a large influx of new services into the China – southern California and China – North Europe corridors during the second quarter, as well as the upgrading of existing strings via the delivery of 12,000+ teu vessels, we forecast that headhaul utilisation factors will be significantly below 90% by July/August. This will not help the implementation of any planned carrier GRIs or peak season surcharges.

It is unlikely we will see any repeat of the lack of space or equipment that was so prevalent last year, which is good news for shippers, but this is not the time to beat carriers down with low rates as this will do nothing to take away the current volatility.

With carriers launching new Asia-Europe and transpacific strings in April and May, it is clear that they are not focused on capacity management and have no intention of laying up tonnage. The market is clearly out of kilter and a correction is required.

The current momentum of the orderbook with recent big orders placed by Maersk, OOCL and Hamburg Sud, together with Greek outsiders joining the party is adding to the feeling of over supply even though the orderbook is currently about 30% of the fleet.

It is not the global supply of ships that is hurting the industry; it is the inability of the operators to deploy their tonnage effectively at the trade route level, combined with the knock on effect of cascading. Slow steaming can no longer absorb so much capacity as every string on the Asia – Europe trade is already switched to this mode.

Neil Dekker, editor of the Container Forecaster said: “A large dose of common sense is needed by the container industry and the direction it takes in the second quarter is in the hands of the carriers.”

Source: Drewry