Tanker Shipping Facing a Tough Year Ahead, Says BIMCO

After a turbulent year, low demand looks set to plague the market in the coming months combined with too many ships fighting for too few cargoes in both the crude oil and oil product segments, says the oil tanker shipping overview and outlook released today by BIMCO.

Demand drivers and freight rates

The realities of the pandemic are setting in for the tanker market. The record-breaking Q2 2020 is a distant memory and, instead, the market faces a slow recovery with low demand, stock drawdowns in consuming countries (with products already where they need to be and therefore not being transported by sea) and loss-making rates.

Perhaps the most notable example of this is on the benchmark Middle East Gulf to China trade where earnings (voyage revenue – voyage costs) have fallen from $250,354 per day in mid-March 2020 to -$1,056 per day on February 15; voyage revenues are so low they no longer cover voyage costs, let alone operating and financing costs. Average earnings for the whole market are slightly better.

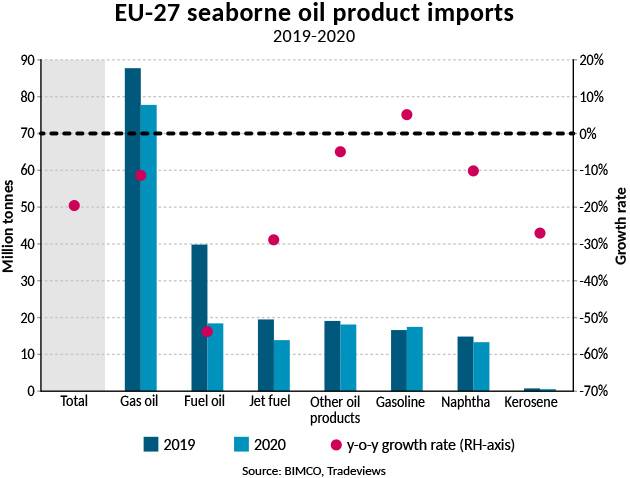

When it comes to cargo demand, oil products were hit in different ways by the crisis; while some are already recovering, others have yet to see any meaningful upturn. Total EU seaborne imports of oil products ended 2020 down by 19.6%, with fuel oil performing the worst, plummeting 53.8% year on year. At the other end of the scale, gasoline imports—accounting for 10.9% of EU seaborne oil product imports—rose 5.1% to 17.4m tonnes. At almost half of total imports, gas oil imports fell to 77.7m tonnes (-11.4%).

Fleet news

At 2.5%, the oil product tanker fleet growth expected by BIMCO is on par with the 2.4% increase in the market experienced in 2020. Crude oil tanker fleet growth is expected to decline from 3.3% in 2020 to 1.5% in 2021, closing in on its low point of 0.9% advance in 2018.

Outlook

The extended OPEC alliance (OPEC+), headed by Saudi Arabia and Russia, went through its up and downs in 2020 and the frailties revealed by the oil price war do not seem to be easily overcome. In early January, the grouping announced that, while Russia would be increasing production in February and March, Saudi Arabia would voluntarily cut its production by 1 million bpd. The different approaches reflect the countries’ focuses, with Russia keen to limit growth in U.S. market share and Saudi Arabia worried about production outpacing demand.

For shipping, if Saudi Arabian exports to China are replaced by Russian crude oil, it is good news, because exports from the Black and Baltic seas have to cover a longer distance than exports from the Middle East.

For more on the report visit: https://www.bimco.org/news-and-trends/market-analysis

![Photo of MT Andaman, [IMO number 9807968] a 30m Indian Navy tug. Converted in 2024 for full uncrewed, remote piloting operation approved by the Indian Register of Shipping.

Image courtesy MDL.](https://images.marinelink.com/images/maritime/w100h100c/photo-of-mt-andaman-imo-170467.jpg)