Geopolitics Dominate the Oil Tanker Market -BIMCO

Developments in the oil tanker market in the past decade dominated by geopolitics, says shipping association BIMCO.

Crude oil and product tanker markets alike have faced high volatility in recent weeks and months, largely due to geopolitics and the constantly evolving situation in the global oil markets. The first major disturbance since the fall in the oil price between the fourth quarter of 2104 and first quarter of 2016 came in the fourth quarter of 2019, after which freight rates have bounced back despite a collapse in demand.

In these extraordinary times, the freight rates are driven by external forces rather than the supply and demand fundamentals of the oil tanker market. However, as the situation slowly begins to normalize, these fundamentals will once again take over with overcapacity being a recurring problem.

Between 2010 and 2019, the cargo carrying capacity of the crude oil tanker fleet grew by 42.2% and the product fleet by 49.5%. This compares to much lower growth in demand over the same period of 6.3% and 18.1% respectively. Overall, the tanker fleet grew by 190.5 million DWT to 622.6 million DWT at the end of 2019. Just under a third are oil product tankers while the rest are crude oil tankers.

“The volatility currently experienced by the tanker market, and the record high freight rates across many of the sectors in particular, dwarfs the ups and downs which were seen in the majority of the previous decade. The market cannot rely on geopolitics to keep rates this elevated in the longer term and the oil tanker market will once again feel the pressure of its poor fundamentals,” says Peter Sand, BIMCO’s Chief Shipping Analyst.

Much longer crude oil hauls as US starts exporting

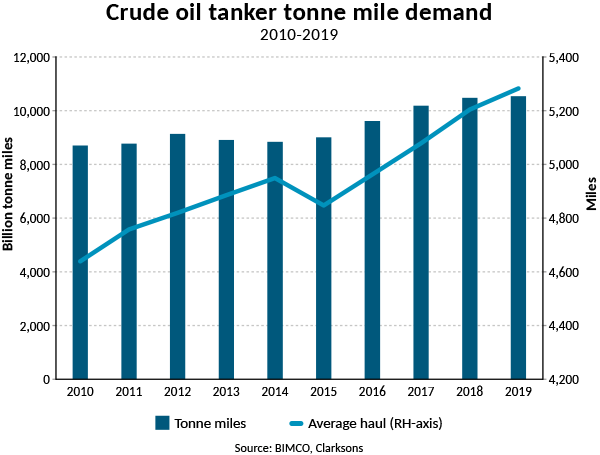

Measured in tonnes, growth in demand for oil product tankers has exceeded demand growth for crude oil tankers, up 18.1% and 6.3% respectively. However, over the course of the decade, the average sailing distance for crude oil tankers has increased, meaning that the 6.3% growth in tonnes has translated into a 21.1% increase in tonne mile demand. Oil product tankers on the other hand, have seen tonne mile demand rise at a slightly slower pace than demand measured in tonnes, as the average sailing distance has decreased slightly.

At the start of the decade, a tonne of crude oil generated an average of 4,640 tonne miles. This number rose by 13.8% over the course of the decade and by 2019, each tonne generated an average of 5,280 tonne miles. The growth in average sailing distance was in part driven by increased crude oil exports from the U.S., which began at the end of 2015 when the crude oil export ban was lifted. As the major importers of crude oil are located in the Far East, the increased share of crude oil coming from the US instead of the Middle East, has increased the average distance sailed. The fall in average haul in 2015 was caused by several developments including higher exports from the Middle East, coupled with lower exports from Africa and lower imports by the U.S.

While demand grew over the decade, three years did experience a fall in total tanker tonne mile demand: down 1% in 2013, down 1.7% in 2014 and a 2.2% drop in 2019. The drops in 2013 and 2014 were large enough to drive demand under 2010 levels in 2014. Strong growth in 2015 and 2016 saw demand back up to levels before the drop.

Only four years saw demand growing faster than the fleet

Comparing demand growth to fleet growth, only four years saw demand grow faster than the fleet;2010, 2016, 2017 and 2018.

The crude oil tanker fleet experienced its highest growth rate in 2011 with 6.5% growth. In absolute terms, 2019 had the largest increase in fleet size, with growth of 6.2% meaning an additional 26.5 million DWT was added to the market that year. Much of this came from the net addition of 63 VLCC tankers to the fleet.

2014 saw the lowest growth, with the fleet growing by just 1.7 million DWT, or just 0.5%. However, as demand fell in 2014, this was yet another year in which the fleet grew faster than demand, worsening the fundamental balance in the oil tanker market.

The oil product tanker fleet saw its highest growth rate in 2010, closely followed by 2016 (both 6.3%). In total, 56.2 million DWT was added to the oil product tanker fleet over the decade. The LR2 fleet has seen the fastest growth by far, up 93.6% over the decade, ending at 44.6 million DWT. The LR1 fleet grew by 31.8% to 27.9 million DWT and the MR fleet, which makes up the majority part of the fleet, grew by 39.6% to 97.3 million DWT.

Profitable decade marred by loss making years

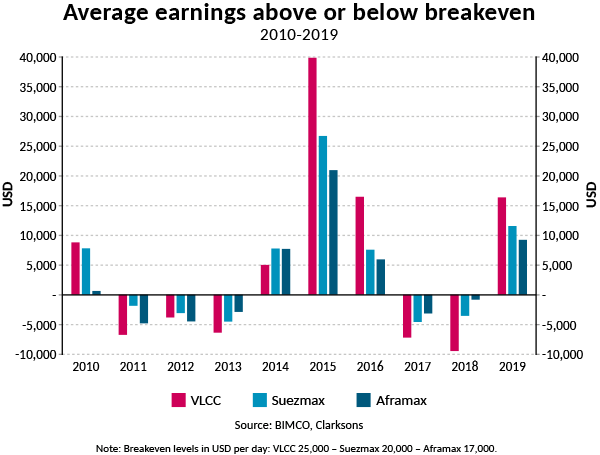

Compared to the freight rates that we have seen these last few weeks and months, those in the previous decade look low, and certainly, earnings did not reach the peaks that we have recently experienced. In the crude oil tanker market, average annual earnings were above breakeven levels half the time for VLCCs and Suezmax ships, whereas Aframax ships saw only four years with average earnings covering both opex and capex costs. BIMCO estimates that a VLCC needs $25,000 per day to breakeven, a Suezmax $20,000 per day and an Aframax $17,000 per day.

A VLCC crude oil tanker earned on average $30,294 per day over the course of the decade, comfortably above the $25,000 per day needed to break even. This illustrates that more money was made in the profitable years than what was lost in those with average earnings below breakeven.

Across all ship sizes, the strongest year for oil product tanker earnings was 2015, with LR2 rates averaging $30,497 per day and MRs $21,405 per day. Over the whole decade, average earnings for an MR tanker stood at $12,377 per day. In comparison, between 2004 and 2008, an MR tanker earned an average of $25,398 per day.

“That the worsening of the fundamental balance was not always reflected in earnings is testament to the fact that, while not as obvious as it has been over these past months, geopolitics have always played an important role in the tanker shipping industry. It will continue to do so in the future, helping to shore up earnings which would otherwise be much lower if solely reflecting the market fundamentals,” Sand says.