Product Tanker Demand Upside Potential; Theory and Reality

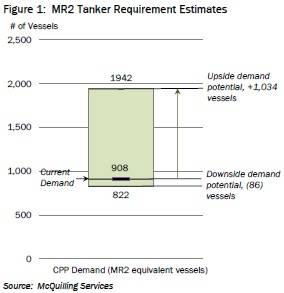

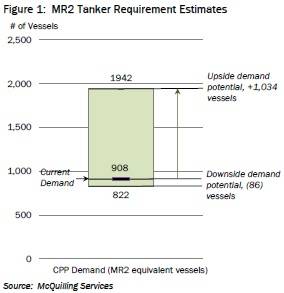

Figure 1 (Source: McQuilling Services)

Figure 1 (Source: McQuilling Services)

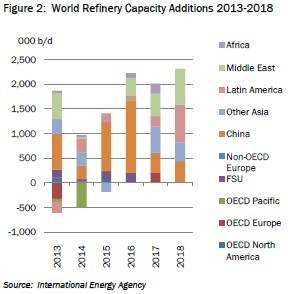

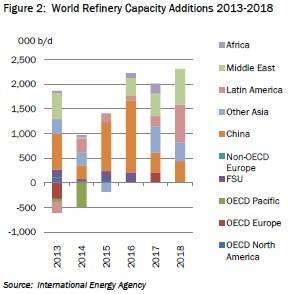

Figure 2 (Source: International Energy Agency)

Figure 2 (Source: International Energy Agency)

McQuilling Services said it continues to hold a contrarian view in contrast with the positive sentiment that surrounds the clean tanker market and robust MR2 ordering.

The company released an industry note outlining their views of the tanker industry.

“In an effort to validate our opinion, we compiled the clean product trade data that was used for McQuilling Services Tanker Market Outlook this year. We arranged the 225 trades (15 x 15 regions) in descending order from the longest to shortest distances, classifying the top 113 trades as long haul trades and the bottom 112 as short haul trades. We calculated the required number of vessels for all 225 trades for one way and round trip voyages based on a sailing speed of 13 knots and eight port days, average deadweight tonnage and historical capacity utilization.

The initial results of this exercise showed that approximately 70% of current clean petroleum product trade is concentrated on the short haul routes in our trade matrix. To reflect the practice of triangulated voyages, we took the average of one way and round trip vessel requirements for all trades. This yielded a base case demand of 908 equivalent MR2 vessels, assuming that all clean product volumes (long and short haul) would be transported solely on this tanker class (Figure 1).

The next step in our exercise was to theoretically assume that all petroleum product volumes would shift to the long or short haul portion of the previously mentioned trade matrix. This step was completed to assess the potential upside of increasing inter-regional trade. Assuming that all trades would evolve from the short to long haul, MR2 demand rose by a strong 114%. This result was driven by the increased leverage in tanker demand (measured in tonmiles), created by longer voyages. We also looked at the case where long haul volumes would shift to short haul, resulting in only a 10% contraction in demand.

While the potential to boost fleet requirements is much greater, the caveat to this part of the exercise is that it is unclear how demand would be distributed across the various vessel classes. Economies of scale would indicate that moving petroleum products across longer distances would support demand for LR2s or LR1s. This would pressure the MR2 requirements utilized for global trade.

Furthermore, the likelihood that this trade evolution will occur appears to be relatively low given the direction of the global economy. This is due to refining infrastructure being built near demand centers, which are located in non-OECD regions. The International Energy Agency (IEA) expects that some 9 million b/d of refining capacity will be added to developing economies between 2013 and 2018. Although some 110,000 b/d (Figure 2) will be removed from OECD Europe’s downstream capacity and some 500,000 b/d from OECD Asia, these regions product demand is also contracting. This will limit large swings in demand for barrels refined further afield.

Furthermore, the slight increase in North American and Former Soviet Union (FSU) downstream capacity could push out some waterborne trade from other regions.

As emerging countries are expected to continue driving oil consumption growth, the potential for the shift towards long haul trades currently appears to be limited. CPP trade should therefore continue to remain concentrated on short haul trades. Another factor that could pressure demand for clean product tankers in the near term is market participants utilizing newly delivered Suezmax tankers to transport cargoes from the Middle East, India or Far East for discharge at ports located West of the Suez Canal. Our proprietary database shows that 12 such voyages have occurred thus far in 2013. This type of fixture could continue to pressure demand for long range product tankers until crude and residual earnings rise, potentially lowering demand for MR2 tankers.

Given these factors, along with the continued ordering activity, we still believe that the clean tanker market could face an oversupply of tonnage in the coming years. Market reports continue to stress the efficiency gains of these orders. However, an oversupply of tonnage will test spot rates, and hence earnings for all tankers, regardless of technical advancements.

Our analysis for this note highlighted the heavy concentration of local trade that is present in clean petroleum product demand. While theoretically possible the potential for these volumes to shift towards interregional trades appears to be relatively low and would in any case benefit larger sized tankers. Given these results, we will remain an outside voice in the chorus of the current market trend until a cacophony of positive earners changes our perspective.”

www.mcquilling.com