Offshore: $11B in Floating Production System Orders Since March ‘11

IMA has completed a study of the floating production market, and the report documents strong growth in the business sector. According to the market survey, 14 floating production units have been ordered over the past four months – a record pace reflecting strong underlying market drivers.

Current Inventory

256 floating production systems are in service or available worldwide. FPSOs comprise 62 percent of the inventory. The balance is comprised of production semis (17 percent), tension leg platforms (9 percent), production spars (7 percent), production barges and FSRUs (5 percent). Of the total production floater inventory, 11 units are currently off field and available for reuse – making the effective utilization rate 95.7 percent.

Recent Orders

The 14 orders since March include the world’s 1st FLNG. At $3 billion the Prelude FLNG is the most expensive floating production unit ordered to date. Among the other orders are nine FPSOs (1 purpose-built unit, 6 units converted from trading tanker hulls and 2 modification/redeployments), 2 production spars and 2 purpose-built FSRUs. Total value of the 14 construction contracts exceeds $11 billion.

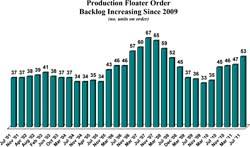

Current order backlog consists of 53 production floaters, a net increase of 6 units since March. This extends the buildup in backlog that began in second half 2009. 28 units utilize purpose built hulls, 25 are based on converted tanker hulls. 20 units are being built for leasing operators, 33 directly for field operators.

Planned Projects

In the report IMA identifies 196 projects in the bidding, design or planning stage that potentially require a floating production or storage system. These projects are declared discoveries or planned developments where a floating production or storage system is being considered as the development option.

Brazil is the most active region for future projects, with 50 potential floater projects in the planning cycle. Next in line is Southeast Asia with 37 projects, followed by West Africa with 36 projects, Northern Europe 22 projects, Gulf of Mexico 17 projects and Australia 11 projects. Of the 196 planned projects, 53 are in the bidding or final design stage. Major hardware contracts for these projects are likely to be awarded within the next 12 to 18 months. Another 143 floater projects are in the planning or study phase. Major hardware contracts for these projects are likely in the 2013 to 2018 timeframe

According to Jim McCaul, head of IMA, “the fundamentals driving the floating production market are extremely strong. World oil demand is growing 1.5 to 2.0% annually, supply disruption remains a major concern, new sources of oil supply need to be developed, oil prices are in the $100 range, deepwater drill rig supply is growing and oil companies are committing an increasing portion of E&P spending to deepwater projects.”

McCaul adds “few if any business sectors can match the dynamism, growth predictability and investment attractiveness of the floating production market.”