How Specialty Lenders Can Propel Marine Operators

Eric Dusch

Eric Dusch

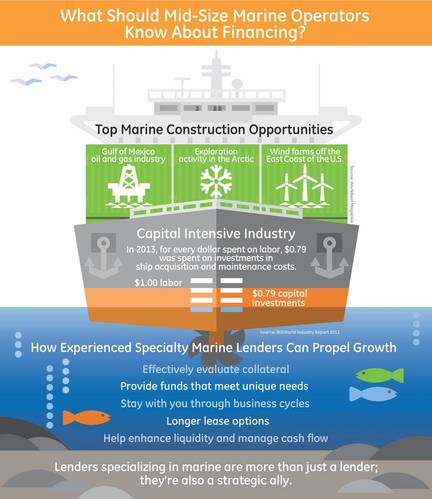

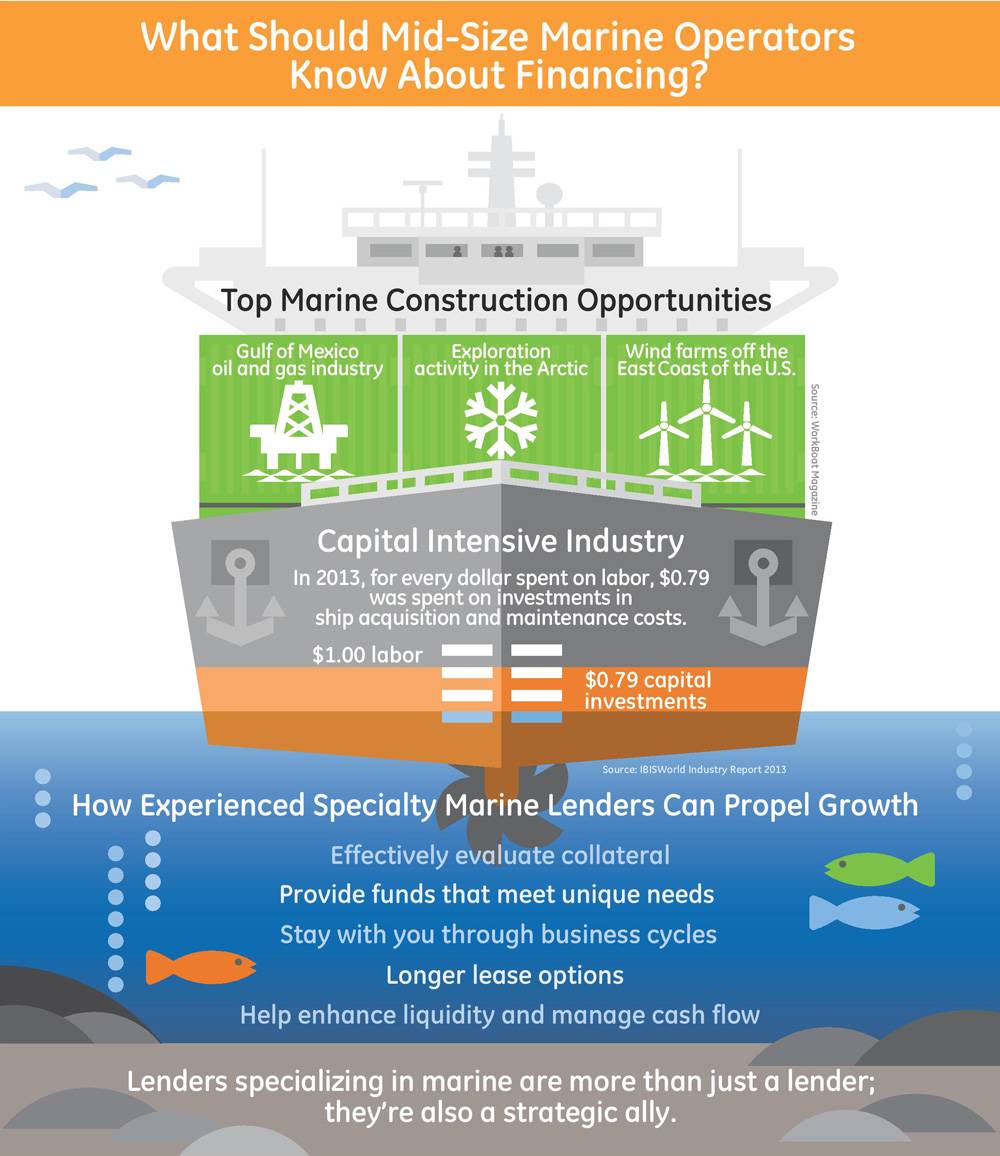

The surge in the shale gas industry in the U.S., as well as stepped up oil exploration in the Gulf of Mexico, is creating enormous demand for marine assets to transport fuels and supplies. To seize this growth opportunity, mid-size marine operating companies with annual revenues from $10 million to $1 billion must address several important issues.

First, what is the most efficient way to finance equipment to keep up with the robust demand? Is ownership of the vessel through a loan structure the best option, or would a lease make better use of working capital? Another issue that operators face is how to evaluate the wave of marine lenders now entering the market and vying for their business. It’s more critical than ever to consider a lender’s depth of knowledge and experience in the industry to get the best possible financing and long-term financial ally.

The Collateral Equation

Marine collateral can be varied and can be difficult for inexperienced lenders to value. These assets include inland towboats and ocean tugs, inland and ocean barges, marine construction equipment and offshore oilfield services. Adding to the valuation challenge is the absence of an active re-sale market to regularly and transparently value these assets in an open market.

As a result, a specialty lender with deep domain knowledge is going to be more comfortable with the collateral, which often means a higher residual value and thus better pricing for the borrower. A knowledgeable lender may also be willing to finance individual components of the boat, such as a new engine or other technologies, as opposed to only being willing to finance the entire vessel.

Long-Term Commitment

A specialty lender that’s been involved in the marine industry is also more experienced with the industry’s cycles and more likely to stick with a borrower through the entire business cycle. The industry is now booming thanks to oil and gas, but this tight link to the oil and gas industries is a double-edged sword. A mid-size company borrower needs a lender that’s committed to the industry and will not look to exit at the first sign of a downdraft.

Longer Loan Terms

Given all this insight, a specialty lender is likely to offer a wider range of financial products with flexible loan and lease structures and payment terms. That makes the lender better able to match the unique needs and goals of customers whether the company is looking to optimize depreciation, lower monthly payments or monetize assets.

Lending can be ideal for customers with long-life equipment needs, who prefer asset ownership and the associated tax benefits. Typically, borrowers can get 80%–100% advance rates from lenders depending on credit quality.

One facet of the loan structure where a specialty lender can often make a big difference is the term of the loan. For new vessels, many lenders prefer to offer a 3-5 year term loan with a 7-10 year amortization. But specialty lenders are more likely to offer a 7-10 year, full term, full amortization loan for new vessels, allowing the borrower to lock in today’s ultra low interest rates for up to 10 years. With a specialty lender, there’s no adjustment period and no need to redo the loan 3-5 years down the road.

The Lease Option

Many banks don’t offer tax and nontax operating leases because they are uncomfortable owing the asset given the potential risks of costs and accidents. Although specialty lenders will not lease just any marine asset—for example, they typically don’t offer leases on tank barges that carry hazardous material or petroleum products—they are more likely to lease certain marine assets than banks because they are more familiar and comfortable with the assets.

Leasing allows customers to use the equipment without tying up capital by owning it. This helps borrowers to enhance liquidity and manage cash flow. The length of these leases are similar to that of loans, and more specialized marine asset might have a residual closer to 50% after 8-10 years. Most leases include an early buyout option at 3 and 5 years, or a fixed price purchase option at the end of the lease.

Find a Strategic Ally

From a lender’s point of view, marine assets are very attractive for three reasons: they tend to hold or even increase in value over time; also, these deals involve large dollar amounts that can be financed over a longer term than most other assets. That makes it easier for lenders to maintain a more stable portfolio of loans. But mid-size marine operators should be cautious of the newcomers attracted to their industry.

Operators need to weigh the relative strength of potential financial allies very carefully. Deep domain expertise and knowledge of the collateral, length of time in the industry and familiarity with the business cycles and the ability to offer a wide breadth of loan and lease products may outweigh another lender’s willingness to shave a few basis points off a loan. Ideally, a specialty lender is more than just a lender; it’s also a strategic ally to help build the business over the long term.

The Author

Eric Dusch is Chief Commercial Officer—Equipment at GE Capital, Corporate Finance, specializing in providing commercial loans and equipment leases to mid-size companies.

e: [email protected]