Westwood: Record Levels of FPS Throughput Capacity to be Sanctioned in 2022

As we enter the final month of 2022, a review of the floating production system (FPS) market revealed that some E&Ps have been bold with investments in the development of their oil and gas (O&G) reserves, with a total of 1.9 mmboepd (1.3 mmbpd of oil and 3.8 bcfd of gas) of FPS throughput capacity sanctioned year to date (YTD).

This represents a 7% increase on 2021, with Westwood anticipating an additional 180 kboepd of FPS throughput capacity to be sanctioned before the end of the year.

A total of 13 FPS units have been sanctioned YTD, with an estimated engineering, procurement, and construction (EPC) value of $15 billion, a 9% increase year-on-year.

Of these awarded units, ten were floating production, storage and offloading (FPSO) units, three were floating production semi-submersible (FPSS) platforms, whilst no spars nor tension leg platforms (TLPs) were awarded.

Although there has been an increase in total FPS EPC contract award value and throughput capacity sanctioned this year compared to 2021, the inflationary cost environment and global supply chain uncertainties have resulted in some E&Ps opting to delay EPC contract awards for major FPS projects previously planned for 2022.

At the start of 2022, Westwood anticipated 25 FPS units, with an EPC value of $19 billion to be sanctioned this year.

However, delays/changes in development concepts to projects such as Equinor’s Wisting development (Norway), Shell’s Gato do Mato (Brazil), Shell’s Linnorm (Norway), and Santos’ Dorado project (Australia) resulted in a 14% downward revision.

The 2022 FPS EPC award value is now anticipated to close at approximately $16.4 billion, driven by 15 units (eight newbuilds, two conversions and five upgrades/redeployments).

It is pertinent to state that the EPC contract value for Petrobras’ P-80, P-82, and P-83 were higher than initially forecasted, hence, reducing the impact of delayed projects on the 2022 EPC value.

Westwood anticipates an upgrade to Cenovus Energy’s Sea Rose FPSO unit, and an EPC contract for CNOOC’s Deepwater 2 FPSS could still be sanctioned before the end of 2022.

Despite major project delays, 2022 will have the highest FPS throughput capacity sanctioned since 2010.

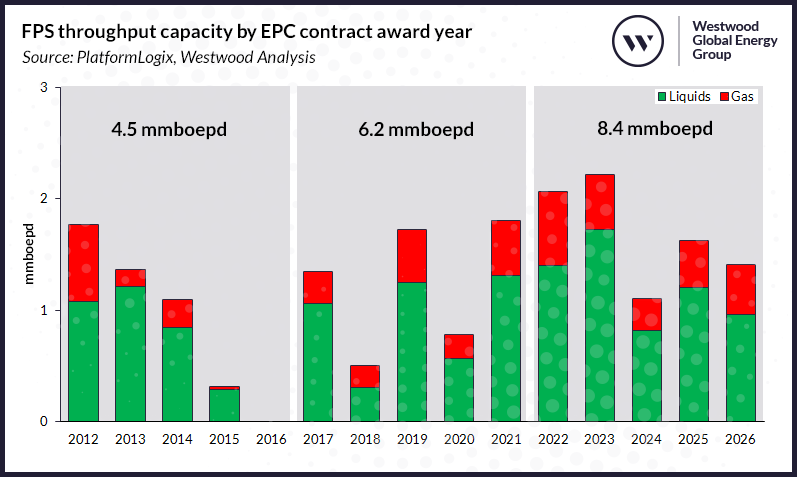

FPS throughput capacity by EPC contract award year Source: PlatformLogix, Westwood Analysis Looking forward to 2023, Westwood estimates FPS throughput capacity to be sanctioned to total 2.2 mmboepd, with an EPC award value of $16 billion.

This is expected to be driven predominantly by activities in Latin America and West Africa.

Major EPC awards anticipated in 2023 include Petrobras’ P-81, P-84 and P-85 FPSOs, as well as Equinor’s Pao de Acucar unit offshore Brazil.

In Guyana, Modec recently signed the front-end engineering and design (FEED) contract for the fifth Stabroek FPSO unit to be deployed on ExxonMobil’s Uaru.

However, the EPCI contract award anticipated in 2023 is subject to governmental approvals of the field development plan and a final investment decision by Exxon.

Other FPS units expected to watch in 2023 include Azule Energy’s Agogo FPSO (Angola), TotalEnergies’ Cameia FPSO (Angola), Eni’s Baleine FPSO (Ivory Coast), and Woodside Energy’s Trion FPSS (Mexico).

Woodside expects bid submission for the Trion unit in 1Q 2023 after the operator delayed FID from 2022, citing the need to optimize the development and execution plan, cost, and development schedule. Supply chain inflationary pressure remains a concern.

Over the past five years, cost deflation, simplification, and standardization have seen the EPC cost of FPSO units fall dramatically, averaging $7,950/boepd of throughput capacity.

This is a 38% discount compared to the highs of $12,795/boepd observed over the 2013/14 period.

However, an increase in the volume of active EPC tenders and an uptick in industry cost has resulted in average 2022 EPC costs of $9,310/boepd.

This represents a 17% increase over the 2017-2021 period and a 32% increase compared to activities in 2020 during the peak of the Covid-19 pandemic.

Considering five-year contracting periods between 2012 and 2026, forecast FPS throughput capacity to be sanctioned over the 2022-2026 period represents a 36% increase compared to the preceding five-year period and an 87% growth on the 2012-2016 period.

However, rising costs are causing significant delays to major projects. Furthermore, concerns over shipyard capacity remain, as China’s ‘Zero-Covid’ policy could exacerbate supply chain constraints following uncertainties created due to the war in Ukraine.

Should an uptick in industry costs continue, previously delayed projects such as Equinor’s Rosebank (UK) and Bay Du Nord development (Canada), Shell’s Bonga SW (Nigeria) and TotalEnergies’ Block 58 development could experience further delays, thereby impacting the total FPS throughput capacity to be sanctioned over the forecast period.