Chemical Shipping Freight Rates to Remain Under Pressure

On the back of low bunker prices and more new buildings to be delivered in 2016, chemical shipping freight rates for both contracts of affreightment and spot cargoes will be under pressure throughout 2016, as there are some new operators looking to break into the long-haul trade routes, according to the latest edition of the Chemical Forecaster, published by global shipping consultancy Drewry.

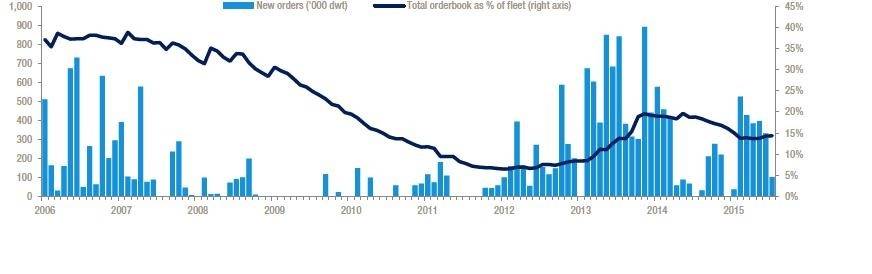

More and more larger vessels were delivered during 2015; a total of 193 ships, aggregating 7.4 million dwt with an average vessel size of 38,390 dwt hit the water during the year. About 206 ships totalling 3.72 million dwt and averaging 18,058 dwt were removed from the fleet.

The stainless steel orderbook is at 37% of the number of ships and 41% of the existing deadweight. Although some of the older stainless/coated ships will likely be scrapped over the next year or two, the fully stainless fleet is very young and the number of deletions will be very small in relation to deliveries.

“Shipyards still have the capacity to build more chemical tankers and we expect many ships to be ordered this year for delivery in 2017 and beyond. None of this leaves us optimistic about the future of the chemical tanker industry and our outlook for this segment is quite bleak,” said Drewry’s Lead Analyst for Chemical Shipping Hu Qing.

El Nino brought dry weather across South-East Asia, affecting the palm oil producing countries of Malaysia and Indonesia by lowering yields and output. With prolonged dry weather caused by the August 2015 drought and the effects of El Nino, production is likely to decline substantially in 2016.

“We expect spot activity out of the Middle East and US Gulf to increase significantly in 2016, but freight rates for both contracts of affreightment and spot cargoes will remain under pressure throughout the year, as there are some new operators looking to break into the long-haul trade routes,” added Qing.