Updated Forecast: Floating Production System Orders

© ggw / Adobe Stock

© ggw / Adobe Stock

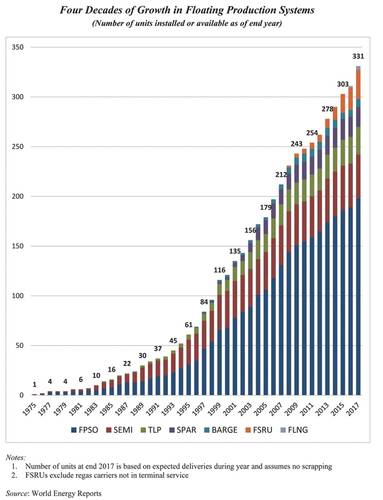

Source: World Energy Reports

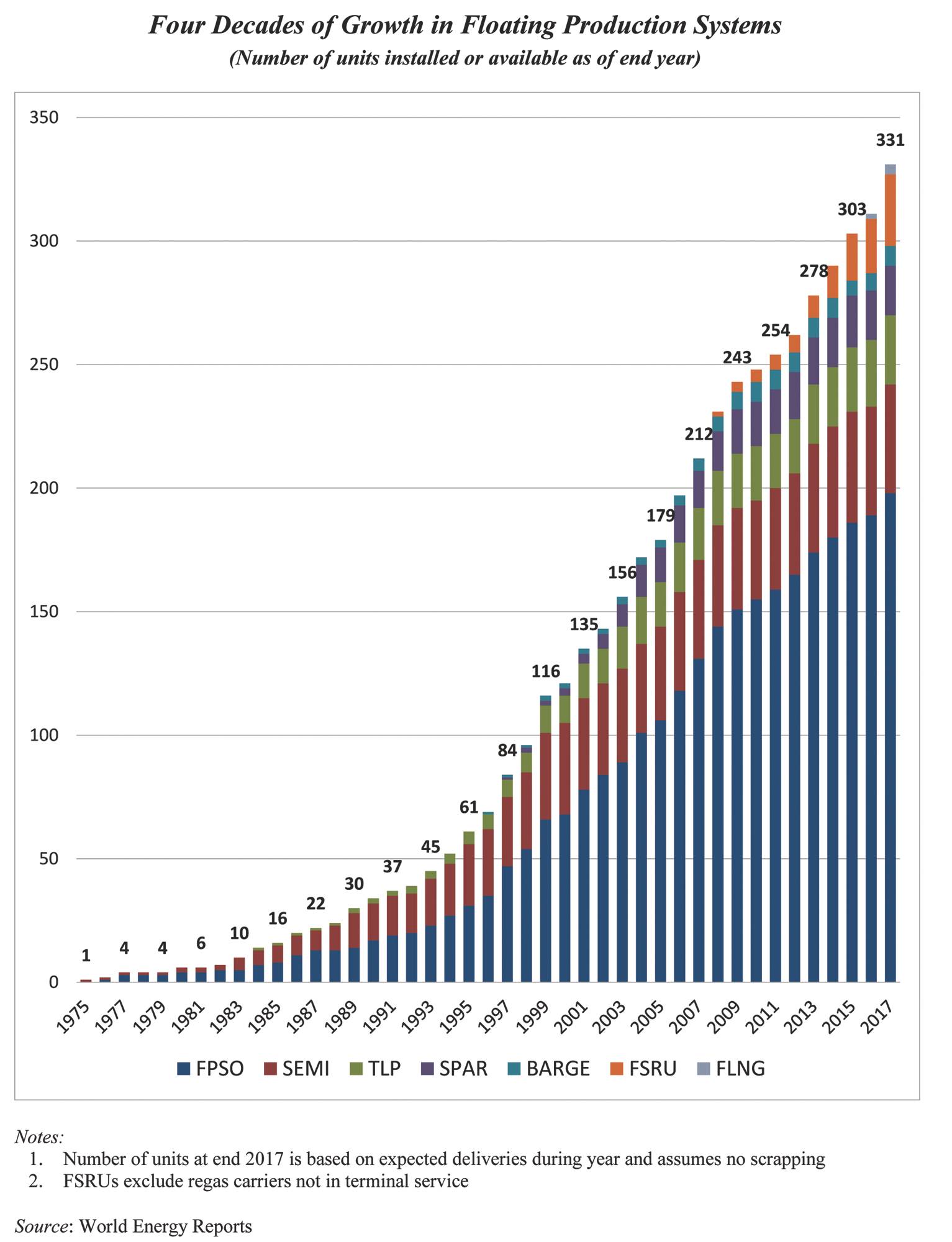

Source: World Energy Reports

World Energy Reports has released its midterm five year forecast of production floater orders. The forecast, detailed in the March 2017 WER report, reflects positive and negative developments in underlying business drivers since WER’s five year forecast last October.

Positive developments

- Likelihood that the November U.S. election results will accelerate U.S. deepwater E&D – the new industry-friendly administration is cutting environmental barriers, opening new areas to E&D and plans tax cuts to encourage domestic energy development

- Faster pace of rebound in oil company capital spending – ExxonMobil, BP, Hess have increased their capex budget for E&D in 2017, reflecting a more bullish near-term outlook for capital spending than apparent last October

Negative developments

- Downturn in expected oil prices – while spot crude prices have increased due to the OPEC cuts, the futures market in March sees Brent crude for delivery five years out trading 10 percent lower than the projected prices last October

- Continued inability of Petrobras to regain traction following the corruption scandal – opposition to local content flexibility has delayed procurement of new FPSOs, legal challenges have prevented the sale of assets to improve cash position

- More rapid expected increase in cost of capital – U.S. Fed targeting of three or four quarter point increases in the overnight lending rate within this year and likely similar tightening by other central banks will make deepwater projects more expensive

Overall, the net impact of these changes is slightly negative – but the outlook for a ramp up in production floater orders remains bullish. We now anticipate orders for 32 FPSOs and eight FPUs over the 2017/21 time period – two fewer units than the October forecast. The reduction is the result of several FPSO orders being pushed beyond the five year forecast window. Similar to our October forecast, we continue to anticipate orders for 25 LNG regasification floaters and around 25 FSOs over the next five years.

In the March report is a list of 73 FPSO/FPU projects that have potential to move to the development stage through end-2021. They are all announced discoveries capable of moving to the EPC contracting stage over the next five years – i.e., a physical backlog of potential project starts. The projects are segmented into three time periods for possible investment decision – within the next 18 months, next 18 to 36 months and 36 to 60 months out. Of course, timing of the EPC contracting decision depends on the underlying business drivers – and at $50-$55 oil only a portion (approximately 55 percent) are expected to proceed to a FID during the forecast period.

The data section in the report provides details for 199 floater projects in the planning stage, 48 production or storage floaters now on order, 294 floating production units currently in service and 28 production floaters available for redeployment contracts. Charts in the report update the location where floating production and storage systems are being planned, operating, being built and to be installed. Accompanying excel spreadsheets provide the report data in sortable format. Information is current as of March 20.

For more information, contact

Jim McCaul - [email protected] or Jean Vertucci - [email protected]

(As published in the April 2017 edition of Maritime Reporter & Engineering News)