Shipping Confidence Continues to Climb -Report

© weerasak / Adobe Stock

© weerasak / Adobe Stock

Richard Greiner (Photo: Moore Stephens)

Richard Greiner (Photo: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

(Image: Moore Stephens)

A recent survey found that shipping confidence reached its highest rating in the past three years in the three months to end-August 2017.

According to the latest Shipping Confidence Survey from international accountant and shipping adviser Moore Stephens, the average confidence level expressed by respondents to the survey was up slightly from the 6.1 out of 10 recorded in the previous survey in May 2017 to a three-year high of 6.2. The improved rating was attributable mainly to increased confidence on the part of owners, up from 6.1 to 6.5. Confidence levels on the part of brokers, meanwhile, fell from 6.4 to 6.3, while managers and charterers recorded more substantial drops – from 6.2 to 5.8 and from 6.4 to 4.7 respectively, the lowest levels in both cases since May 2016. The survey was launched in May 2008 with an overall confidence rating of 6.8.

Confidence levels were significantly up in Asia from 5.6 to 6.4, their highest level since May 2014. Confidence was also up in Europe, from 6.2 to 6.3, but down in North America, from 6.4 to 5.8.

Despite familiar concerns about excess tonnage capacity in many trades and continuing uncertainty over Brexit, several respondents saw reasons for optimism over the coming 12 months, not least as a result of what one described as “some green shoots of a relatively broad-based rebound in economic activity.” This helped maintain, at a three-year high, expectations of major investments being made over the next 12 months. Concern, however, persisted over political instability, the incipient cost of increased legislation, and the probable entry into the market of low-cost newbuildings.

One respondent said, “The future of the maritime industry will certainly be interesting, but will it also be enjoyable?”

The likelihood of respondents making a major investment or significant development over the next 12 months was unchanged from the previous survey at 5.4 out of a maximum possible score of 10. This represents the highest level achieved since August 2014, and this despite a slight fall this time (from 5.9 to 5.8) in the expectations of owners, and a much larger one (from 6.3 to 4) by charterers. The expectations of respondents in Asia were up, from 5.1 to 5.9, but down in Europe, from 5.4 to 5.2.

As was the case in the May 2017 survey, 50 percent of respondents expected finance costs to increase over the coming year. Owners’ expectations were unchanged at 48 percent, but both managers and charterers (where the figures were up from 57 percent to 62 percent and from 57 percent to 67 percent, respectively) were anticipating dearer finance. Brokers were alone among the main categories of respondent in recording a fall (from 63 percent to 42 percent) in the numbers expecting finance costs to go down.

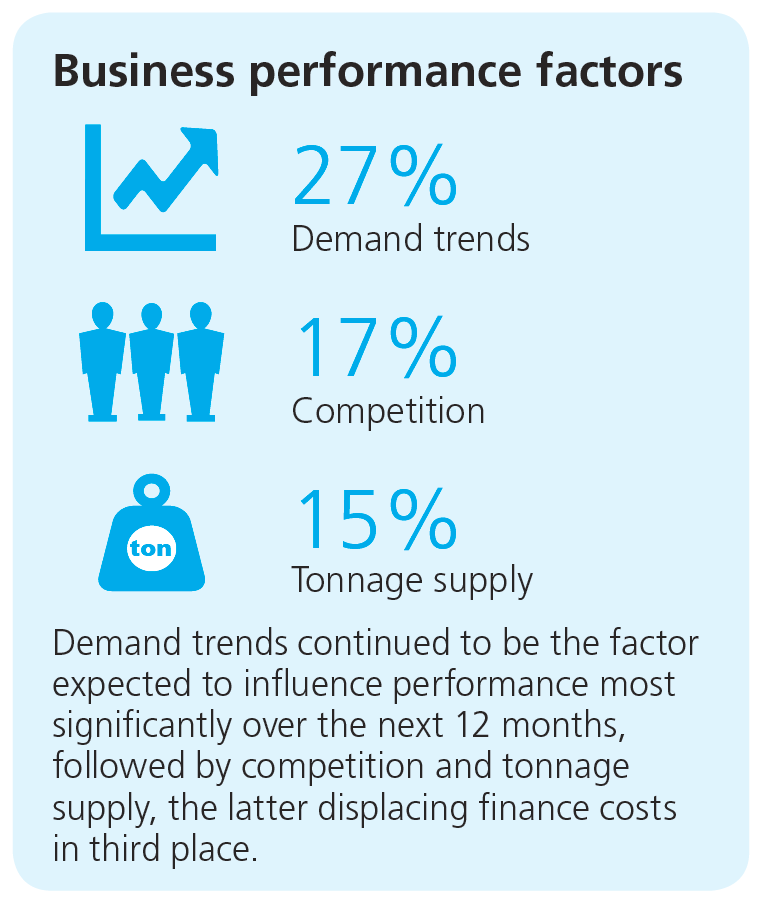

Demand trends, cited by 27 percent of respondents, continued to be the factor expected to influence performance most significantly over the next 12 months, followed by competition (17 percent) and tonnage supply (15 percent), the latter displacing finance costs in third place. One respondent said: “Confidence is impaired by the inexperience of investment houses resulting in over-liquidity in the market, which feels that it has to spend just for the sake of it – a ‘greed-eats-brain’ mentality.”

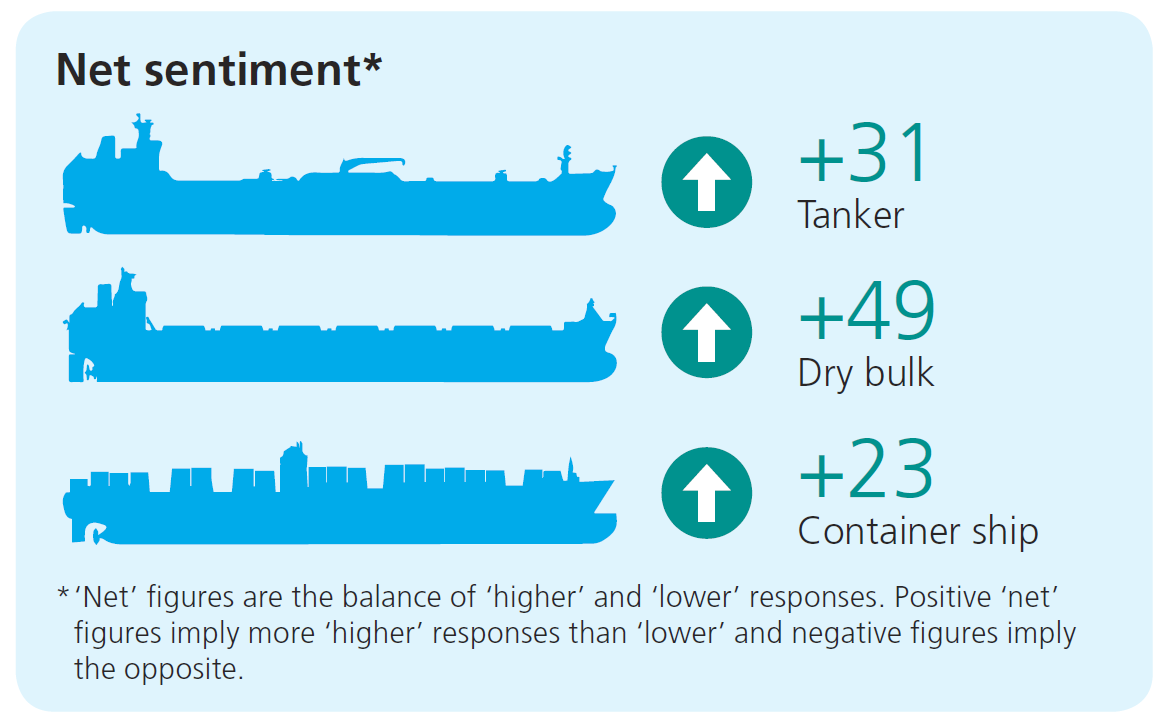

The number of respondents expecting higher rates over the next 12 months in the tanker market was up on the previous survey, from 32 percent to 45 percent, while there was a 2 percent fall, to 14 percent, in those anticipating lower tanker rates. Meanwhile, although there was a two percentage-point fall, to 56 percent, in the numbers anticipating higher rates in the dry bulk sector, this was still the second-highest figure in three-and-a-half years. In the container ship sector, the numbers expecting higher rates dropped by six percentage points to 40 percent, while there was a five percent increase, to 17 percent, in those anticipating lower container ship rates.

Net sentiment was positive in all the main tonnage categories, and up in the tanker market from +16 in May 2017 to +31 this time. There were meanwhile small declines in net sentiment in the dry bulk and container ship trades, from +50 to +49 and from +34 to +23 respectively.

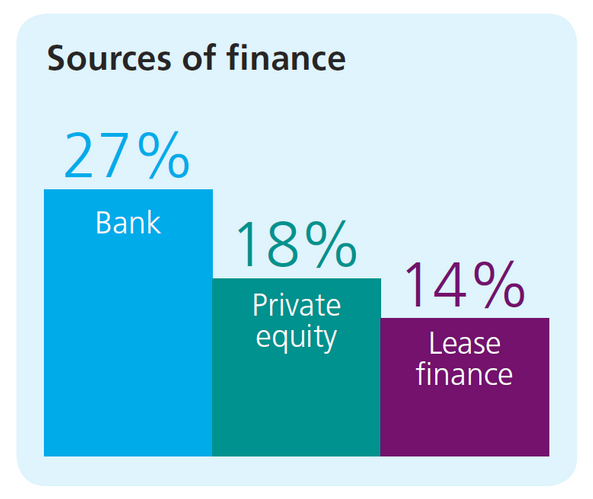

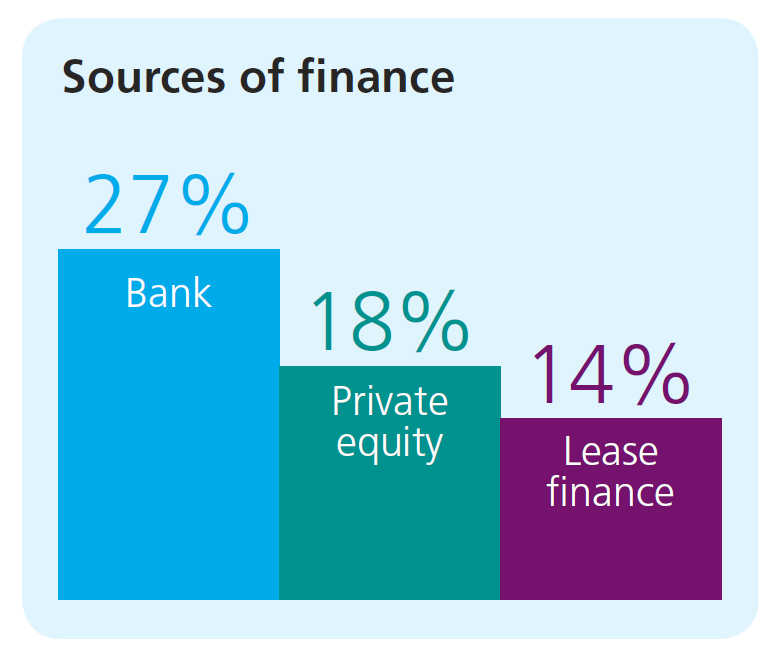

In a standalone question, respondents were asked to rank in order of priority what they considered to be the most significant new sources of finance for shipping over the next 12 months. Bank finance emerged as the first choice of 27 percent of respondents, followed by private equity (18 percent). Lease finance (14 percent) featured in third place, one percentage point ahead of shareholder funds. One respondent said, “Banks are being a lot tougher with owners, and it is good to see the demise of the CV and KG systems which generally did little to help the long-term viability of the industry.” Another observed, “For good owners, there is still capital available. But the worry is for the second and third-rung owners.”

Richard Greiner, Moore Stephens Partner, Shipping & Transports, says, “Another three months, and another rise in confidence in the shipping industry, albeit a small one. Confidence has been increasing steadily over the past 15 months, and industry players are more confident of making a major investment over the coming year than they have been at any time in the past three years. Moreover, net sentiment in all three main tonnage categories is positive, having almost doubled in the tanker sector over the past quarter.

“This welcome boost in confidence comes at a difficult time for the industry, beset by overtonnaging in many trades, the current and impending cost of regulatory compliance, and more widely by geo-political pressures. Clearly, shipping still has a lot to offer existing and new investors alike, both traditional and external.

“To some extent, success in the shipping industry is a question of being in the right place at the right time. But there is a lot of skill, knowledge and experience involved, too. It is good to see that confidence is still on the increase. They do say that it’s the hope that kills you but, in truth, the lack of it is likely to be far more damaging.”