Is Dry Bulk Still on Track for Profitability in 2019?

© Volodymyr Kyrylyuk / Adobe Stock

© Volodymyr Kyrylyuk / Adobe Stock

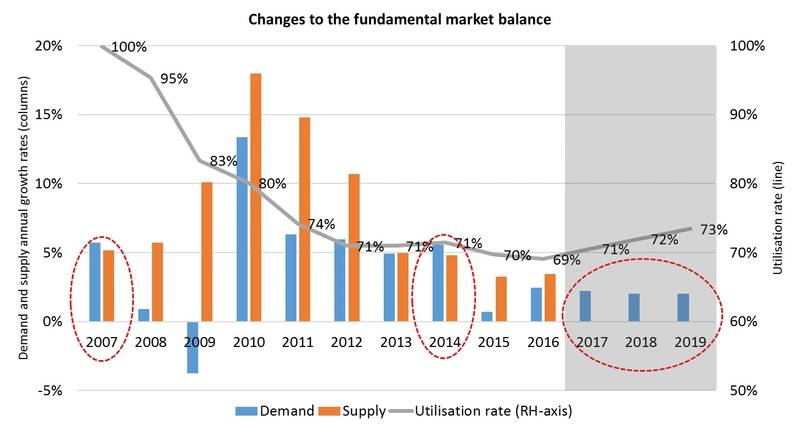

Source: BIMCO estimates (2017-), BIMCO utilization est. (2007-2023), Clarksons demand growth rates (2007-2017) Note: Net supply growth of 0 million DWT in 2017. Demand growth rate of 2.2% in 2017. Note: The years circled are where demand growth outstrips supply growth = improving the market.(Photo: Bimco)

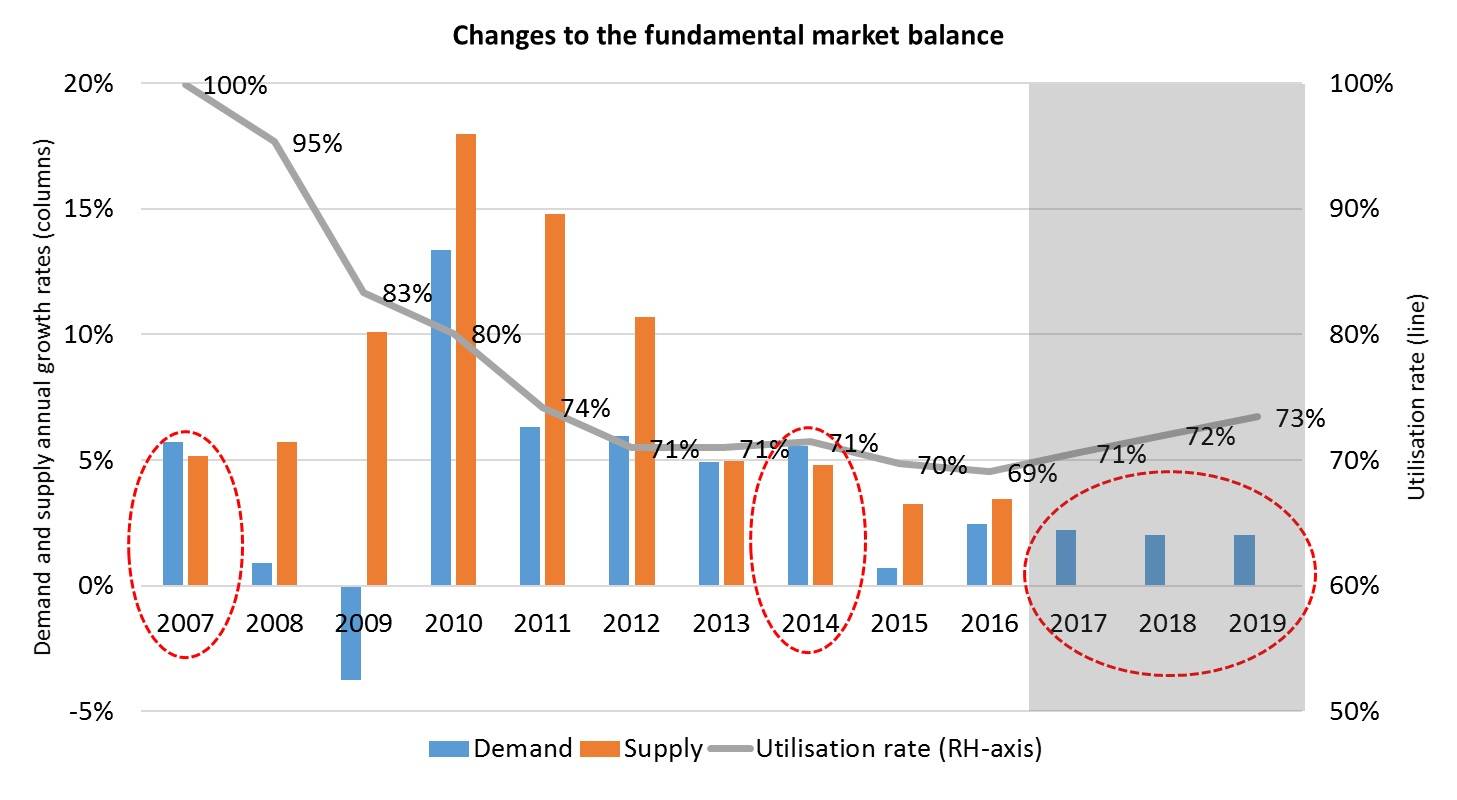

Source: BIMCO estimates (2017-), BIMCO utilization est. (2007-2023), Clarksons demand growth rates (2007-2017) Note: Net supply growth of 0 million DWT in 2017. Demand growth rate of 2.2% in 2017. Note: The years circled are where demand growth outstrips supply growth = improving the market.(Photo: Bimco)

The dry bulk industry remains well on target for profitable freight rates in 2019, according to BIMCO. This relies however, on the projected fleet supply growth rate of 0 percent in 2017 continuing. The handymax segment may even see profits in 2018 as demand may go beyond 2 percent in 2017 before reverting to 2 percent in 2018 onward.

In 2016, the supply side grew by 3 percent and the demand side grew by 2.4 percent measured on a metric-ton-mile basis. This resulted in a worsening of the fundamental market balance. However, as the original “Road to Recovery” in May 2016 projected an even worse fundamental deterioration in 2016 – we are today, in a relatively better position than anticipated nine months ago.

BIMCO’s Chief Shipping Analyst Peter Sand said, “Estimating a return to profitability in the dry bulk industry remains a moving target, and one that differs from one company to the next. But by projecting a course for profitability, everyone in the industry can use it as a reference.

“The fact that the first half of February 2017 was a troublesome period came as no surprise and it makes the strong comeback in the following month stand out as even more remarkable. During that time, the BDI went from 688 to 1,147.

“This lift in freight rates is certainly positive, but there is still work to be done on the supply side. A significant level of demolition activity must be maintained, and increasing focus must also be on keeping slow steaming around.”

What has changed? Besides a relatively better fundamental balance, mostly the daily running costs. The drop in OPEX more than makes up for the fundamental deterioration of the freight market. Speed may also be a factor coming into play as renewed optimism and upwardly moving freight rates are often followed by a less intense focus on maintaining slow steaming.

In total, freight rates will be slightly higher than originally projected for the coming years. Combining the relatively better freight market, with a 10-year-low OPEX level in 2016 – the dry bulk industry remains on the road to recovery.

Even small changes matter

Using the assumptions already mentioned above for the supply and demand side, a further drop in OPEX of 5 percent will also bring profits for the handysize sector in 2018. This will then mean a just-profitable industry in 2018 overall. However, not profitable for all the sub-sectors, as the panamax and capesize sectors are estimated to remain in the red.

Moreover, a higher supply side growth rate than 0 percent in 2017, which BIMCO expect to be the case, may not completely wipe out recovery in 2019. As demand is expected above 2 percent as a target growth in 2017, ‘damage’ from a slip on the supply side is reduced by a stronger demand side.