Western Bulk Returns to Profit

Oslo-listed dry bulk operator Western Bulk reported a marked earnings recovery in the second half of 2025, capitalizing on a broad-based rebound in freight markets and tighter effective vessel supply.According to the company’s Second Half Year Report 2025, Western Bulk generated a net profit after tax of USD 7.4 million in 2H 2025, compared with a net loss of USD 5.2 million in the same period a year earlier. For the full year, the group posted a net profit of USD 5.4 million…

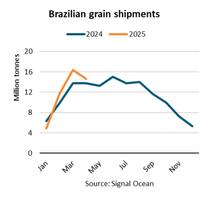

BIMCO: Brazilian Grain Shipments Up 9% as China Seeks US Alternative

Between January and April 2025, Brazilian grain shipments rose 9% y/y, supported by strong Chinese purchasing, according to Filipe Gouveia, Shipping Analysis Manager at BIMCO.The ramp-up in exports has been supported by a 9% increase in the soya bean harvest, according to estimates by the United States Department of Agriculture (USDA). Shipments were weakest in January due to a delay in the harvest, but they quickly ramped up in February, driving an increase in ship congestion.

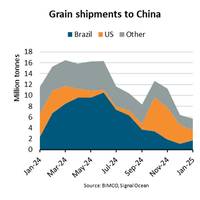

China Grain Imports Plummet 51%

“In January, grain shipments to China are estimated to fall 51% y/y, partly due to a decline in import demand for soya beans caused by low crusher margins. Although Chinese soya bean production decreased 1% y/y in 2024, inventories are high after a surge in imports in the first half of the year. Import demand for maize and wheat has also declined due to record high harvests in China in 2024,” says Filipe Gouveia, Shipping Analysis Manager at BIMCO.As the world’s largest grain importer, China has for a long time strived to reduce its import dependence.

Castor Maritime Adds 2020-built Bulk Carrier

Castor Maritime announced that on October 9, 2024, it took delivery of the M/V Magic Ariel, the 2020-built Kamsarmax bulk carrier vessel it had agreed to acquire as previously announced on September 30, 2024.The vessel acquisition was financed in its entirety with cash on hand.The Magic Ariel will be employed under a time charter contract with a minimum duration of about seven months at a gross daily rate equal to 108% of the Baltic Panamax Index 5TC (BPI5TC).

Capesize Bulker Rates See Best Day in Over Two Years

The Baltic Exchange's main sea freight index, tracking rates for ships carrying dry bulk commodities, rose on Thursday after rates for bigger vessel segments snapped their losing streaks, with capesize seeing its best day in over two years.The overall index, which factors in rates for capesize, panamax, supramax shipping vessels, was up 37 points, or 3.8%, at 1,002 points.

Castor Maritime Announces New Charter Agreements

Shipping company Castor Maritime on Monday announced it has lined up time charter contracts for three of its bulk carriers. The Magic Moon, a 2005 built Panamax dry bulk carrier, has been fixed on a time charter contract at a gross daily charter rate of $25,500. The charter commenced on April 7, 2022, and has a duration of about 25 days.The Magic Rainbow, a 2007 built Panamax dry bulk carrier, has been fixed on a time charter contract at a gross daily charter rate of $16,500. The charter commenced on April 12, 2022, and has a duration of about 60 days.The Magic Horizon, a 2010 built Panamax dry bulk carrier, has been fixed on a time charter contract at a gross daily charter rate of $17,500. The charter commenced on April 15, 2022, and has a duration of about 55 days.

Castor Maritime Lines Up New Charter Agreements

Shipping company Castor Maritime Inc. announced it has secured charter agreements for several of its bulk carriers. The Magic Moon, a 2005 built Panamax dry bulk carrier, has been fixed on a time charter contract at a gross daily charter rate of $25,000. The charter commenced on March 6, 2022, and has a minimum duration of about 30 days.The Magic Argo, a 2009 built Kamsarmax dry bulk carrier, has been fixed on a time charter contract at a gross daily charter rate equal to 103% of the average of the Baltic Panamax Index 5TC routes. The charter is expected to commence on April 4, 2022, and will have a minimum duration of twelve months and a maximum duration of fifteen months at the charterer’s option.The Magic Venus…

Castor Maritime Announces New Charter Agreements

Cyprus-based shipping company Castor Maritime Inc. announced it has secured new charter agreements for several of its bulk carrier vessels.The 2010-built Panamax dry bulk carrier Magic Nova has been fixed on a time charter contract at a gross daily charter rate equal to 92% of the average of the Baltic Panamax Index 5TC routes. The charter commenced on November 17, 2021, and has a minimum duration of eleven months and a maximum duration of about fourteen months (+/- 15 days) at the charterer’s option.The 2006-built Capesize dry bulk carrier Magic Orion has been fixed on a time charter contract at a gross daily charter rate equal to 101% of the average of the Baltic Capesize Index 5TC routes.

Navios Announces Delivery of Three Vessels

Navios Maritime Partners L.P., an owner and operator of dry cargo vessels, has taken delivery of the following three drybulk vessels: Navios Amitie - a 2021-built, Kamsarmax vessel with 82,002 dwt, was delivered into Navios Partners’ fleet on May 28, 2021. The vessel is chartered out at a rate of 110% of average Baltic Panamax Index (BPI 82) until May 2024. Based on BPI 82 weighted time charter average as of June 10, 2021, the vessel would earn approximately $31,720 per day. Navios Star – a 2021-built Kamsarmax vessel with 82,037 dwt, was delivered into Navios Partners’ fleet on June 10, 2021. The vessel is chartered out at a rate of 110% of average Baltic Panamax Index (BPI 82) until June 2024.

Castor Maritime Buys 2015-built Dry Bulk Carrier

Cyprus-based shipping company Castor Maritime has agreed to acquire a 2015 Chinese-built Kamsarmax dry bulk carrier from an unaffiliated third party for $23.5 million. The vessel comes with a charter contract included."The vessel will be delivered to the Company with a time charter contract attached with a reputable charterer, at a daily gross charter rate equal to 114% of the Baltic Panamax Index, and with an estimated remaining term of about 17 to 21 months," Castor Maritime…

Baltic Index Slips with Falling Panamax Rates, Capesize Revives

The Baltic Exchange's main sea freight index, which tracks rates for ships carrying dry bulk commodities, fell further on Wednesday, dragged down by decreasing panamax rates. The overall index, which factors in average daily earnings of capesize, panamax, supramax and handysize dry bulk transport vessels, shed 6 points, or 0.76 percent, to 782 points. The Baltic's capesize index inched up 2 points, or 0.42 percent, to 474 points - the first upward movement since November 21, after the index hit its lowest on record on Tuesday, according to data available on the Baltic Exchange website that dates back to March 1999. Average daily earnings for capesize vessels rose on Wednesday, settling up $35 at $4,945.

Excel Maritime Enters Time Charters

Excel Maritime Carriers Ltd (NYSE: EXM), an owner and operator of dry bulk carriers and provider of seaborne transportation services for dry bulk cargoes, announced today that it has entered into two two-year time charters for its Kamsarmax vessels M/V Coal Hunter and M/V Santa Barbara. M/V Coal Hunter and M/V Santa Barbara are both 2006-built Kamsarmax bulk carriers with carrying capacity of 82,298 and 82,266 dwt respectively. The vessels have been fixed under separate time charters with European charterers for a period of two years at a gross daily charter rate of $15,000 for the first year. The daily rate for the second year will be linked to the Baltic Panamax Index (BPI) with guaranteed minimum rate (floor) at $14,000 per day and a profit sharing arrangement.

Seanergy Maritime Q3 & Nine Month Report

Seanergy Maritime Holdings Corp. (NASDAQ: SHIP; SHIP.W) announced its operating results for the third quarter and nine months ended September 30, 2010. Dale Ploughman, the company’s Chief Executive Officer, stated: “The third quarter of 2010 was another important quarter in our development as we completed successfully the acquisition of the remaining 49% ownership interest in Maritime Capital Shipping Limited (“MCS”). In addition, on October 22, 2010 we completed the acquisition of the remaining 50% ownership interest in Bulk Energy Transport (Holdings) Limited (“BET”) and, as a result, we now own 100% of MCS and BET and their fleets.

Navios Maritime Partners Results for Q2 2010

Navios Maritime Partners L.P. (NYSE: NMM), an owner and operator of dry cargo vessels, reported its financial results for the second quarter and six months ended June 30, 2010. Angeliki Frangou, Chairman and Chief Executive Officer of Navios Partners, stated: "I am pleased with our performance during the second quarter. We raised $92.3 million in the equity markets and purchased the Navios Pollux. The acquisition of the Navios Pollux increases the average charter coverage of our fleet to 4.4 years and reduces the average age of our fleet to 5.7 years. Throughout this release, EBITDA for the three and six months ended June 30, 2009 represents net income before interest…

Dry Bulk Trends

The dry cargo freight market was generally little changed last week, with Capesize conditions remaining basically steady but quiet, brokers said. Panamax activity was brisk from South America, but rates failed to advance as rapidly as owners had hoped for, they added. However, some firmer rates were seen, with Cosco's fixture of a 1990-built 74,000 dwt vessel delivery north Brazil trip China at $11,500 daily plus a $250,000 ballast bonus. Dreyfus was also active and paid a firmer $10,250 daily plus $265,000 ballast bonus for 1991-built Sea Ilex 66,000 dwt delivery Plate April 5/10 trip Continent. On March 28, the Baltic Dry Index (BDI) rose four points to 1…

BDI Up 9

The Baltic Dry Index (BDI) rose nine points to 1,660, the Baltic Panamax Index gained four points to 1,557, the Baltic Handy Index firmed six points to 1,157, and the Baltic Capesize Index jumped up 17 points to 2,275.

Capesize Rates Ease

Easier conditions were seen for Capesizes in the Atlantic sector of the dry cargo freight market, brokers said last week. Some brokers believed that the gap between Capesize and Panamax rates could not be sustained and that some Capesize cargoes would be split into Panamax sizes. However, it was pointed out that Capesize contracts did not always permit this. Panamax rates were generally unchanged, while Handysize levels remained firm in the East and were said to be stronger from the east coast of South America. The Baltic Dry Index (BDI) was down two points at 1,684, the Baltic Panamax Index fell seven points to 1,513, the Baltic Capesize Index was unchanged at 2,369 and the Baltic Handy Index gained two to 1,181.

Bulk Carrier Trends: Panamax Activity On The Rise

The dry cargo freight market was enlivened by a higher degree of Panamax activity in most areas, while Capesize conditions remained subdued with little fresh business quoted and few fixtures reported, brokers said. On May 9, the Baltic Dry Index gained 2 points from the day before to 1,609, the Baltic Panamax Index rose 11 to 1,512 and the Baltic Handy Index gained one to 1,153, while the Baltic Capesize Index fell six to 2,171. In the grain sector, higher rates were fixed from the Atlantic to the Far East, brokers said. Although brokers were disappointed at the level obtained by the 1999-built Red Cherry 73,350 dwt from Hanjin delivery U.S. Gulf end May trip Far East at $11,200 daily plus a $230,000 ballast bonus, other fixtures were concluded at more generous levels.

Dry Freight Markets Steady

Conditions on the dry cargo freight market were generally steadier for Capesizes on Wednesday, with the Baltic Cape Index posted at an unchanged 2,171, brokers said. Atlantic Panamax rates rose further and brokers said conditions were also slowly improving for owners in the East for later May positions. The South African sector remained firm. The Baltic Dry Index (BDI) gained two points to 1,611 and the Baltic Panamax Index rose 10 points to 1,522, while the Baltic Handysize Index fell three points to 1,150.

Dry Cargo Rates Continue Rise In Quiet Market

Dry cargo rates continued to rise on Tuesday, but the market was quiet following Monday's Labor Day holiday in the U.S., brokers said. Cargill chartered the Ken Pan built in 1984 to ship 31,000 tons of maize from Durban to Japan 10/20 September at $22.75. The Baltic Dry Index (BDI) rose five points to 1,671, the Baltic Panamax Index four points to 1,616, the Baltic Handy Index six points to 1,169 and the Baltic Capesize Index by seven points to 2,239.

Dry Bulk Markets Lower

The Baltic Dry Index (BDI) shed seven points to 1,701, the Baltic Panamax Index (BPI) eased four points points to 1,520, the Baltic Handy Index (BHI) dropped eight points to 1,090, the Baltic Handymax Index fell 42 points to 9,631 and the Baltic Capesize Index (BCI) fell eight pionts to 2,504.

Grain Trading Is Quiet

Grain fixing for Iran continued to hold interest in an otherwise quiet sector, brokers said on Monday. IRISL fixed unnamed tonnage to lift 50,000 tons wheat from St. Lawrence for Iran at $21 with shipment set for December 1/20. This compared with the $21.25 that they paid for 60,000 tons wheat on the same route on November 17 and $20.50-22.00 for two other cargoes of 60,000 tons each on November 16. Tradigrain booked 55,000 tons wheat to Iran but from Kalundborg November 25/30 shipment at $18.25. Cargill was seen fixing cargoes in the grain sector, with 60,000 tons and 55,000 tons heavy grain booked from the U.S. Gulf to Seaforth, England, and Barcelona respectively. Both were concluded at $13.50 and with shipment set for November.

BDI Down Slightly

The Baltic Dry Index (BDI) shed two points to 1,594, the Baltic Panamax Index (BPI) gained five points to 1,573, the Baltic Handymax Index fell 32 points to 9,311 and the Baltic Capesize Index (BCI) was down nine points to 2,173.